Crypto Tax Compliance in 2026: Laws and Scam Risks Explained

- Cryptocurrency

- Updated On: April 16, 2026

Table of Contents

Crypto is now part of the financial system, and in 2026, the rules around it are much stricter. If you buy, sell, or trade crypto, you are expected to report it correctly.

Many people are still unsure about how these rules work. A report by Wolters Kluwer notes that cryptocurrency tax compliance remains a major challenge, mainly because regulations keep changing, and users often lack clear guidance. This confusion does not just lead to mistakes; it also creates risk.

Today, many users first notice a problem when they try to withdraw funds from a platform. They are suddenly asked to pay a “tax” or “clearance fee” upfront. In many cases, these demands come from fake crypto platforms, not real authorities. These are known as fake crypto tax payment scams, and they are becoming more common.

At the same time, real governments are introducing new tax rules for 2026. There is better tracking, stricter reporting, and closer monitoring of transactions across exchanges.

This means users now face two challenges:

- Understanding and following real crypto tax laws

- Avoiding fake tax demands designed to steal funds

In the next section, we’ll break down what has actually changed in crypto tax rules in 2026 and what it means for you.

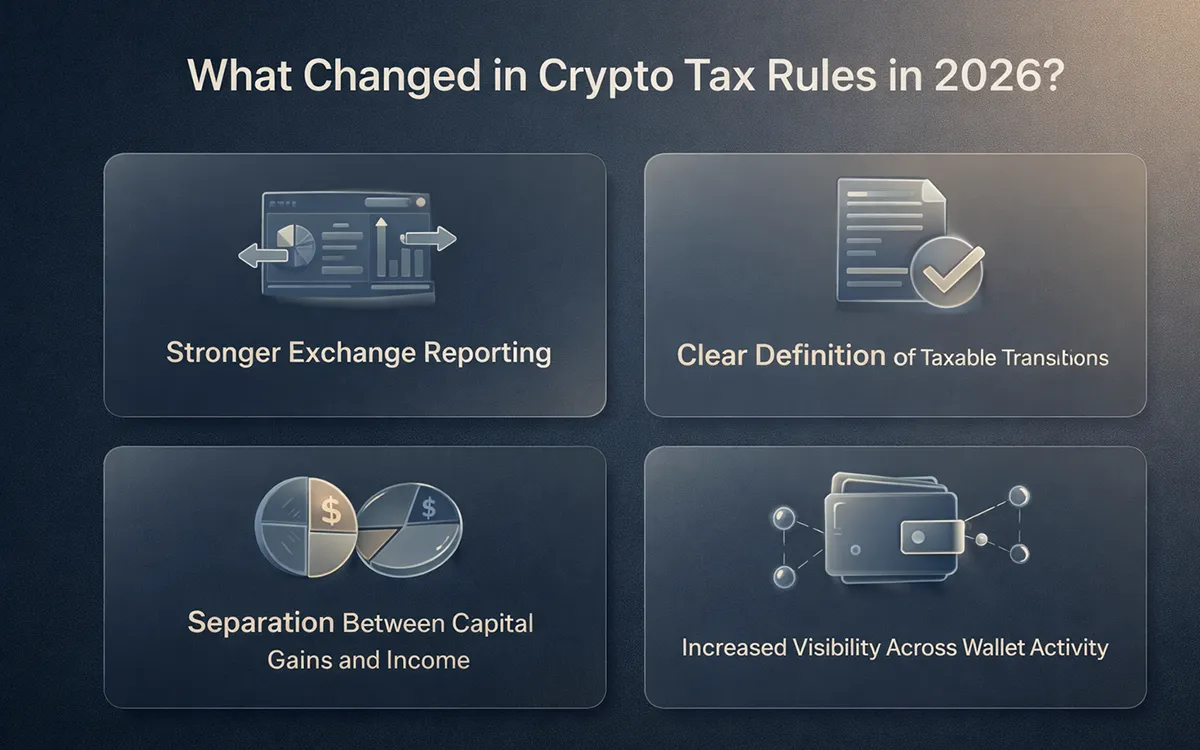

What Changed in Crypto Tax Rules in 2026?

Crypto tax rules in 2026 are no longer unclear or loosely followed. Reporting is now more direct, and expectations are clearly defined. Authorities are focusing on one thing: making sure all crypto activity is properly reported and easy to track.

Here are the key changes you need to understand:

-

More Detailed Transaction Reporting

Crypto exchanges have started mandating their users to report transaction details to tax authorities, including trades, sales, and even deposits and withdrawals from the exchange account.

In the United States, the changes in the reporting requirements of brokers will make it similar to the traditional finance system. This implies that your transactions will be more transparent, leaving less space for discrepancies between reports provided by you and those obtained by the authority.

-

Definition of Cryptocurrency Activities

There is now more understanding about the types of activities that should be reported. The sale of cryptocurrency assets, exchange from one crypto to another, and payment of goods and services via crypto are all taxable transactions.

Moreover, income earned through staking rewards and airdrops is also considered taxable income.

-

Capital Gains versus Income Separation

Now there is an evident separation between capital gains and income related to crypto transactions. Rewards, payments, and bonuses in crypto are regarded as income.

In case that crypto is later sold or spent, it will trigger either capital gains or capital losses. It means that the same crypto asset may be subject to taxation twice. This follows guidance from the Internal Revenue Service.

-

Visibility on Transactions Between Wallets

Monitoring technologies have been developed to facilitate monitoring crypto transactions between wallets.

Transferring crypto to other wallets under one's control is not a taxable action, but it doesn’t make tracking obligations disappear. Once the crypto is sold or utilized, all its transactions will be accounted for.

These updates make cryptocurrency tax compliance more important than before. Errors or missing details are easier to spot. At the same time, confusion around these rules is increasing. This is often used by fake crypto platforms that introduce upfront “tax payments” during withdrawals. Understanding the real rules helps you avoid both penalties and scams.

Cryptocurrency Tax Compliance: What You Must Do

Understanding the rules is one part. Following them correctly is what keeps you safe from penalties.

Here’s how to handle cryptocurrency tax compliance in 2026:

-

Maintain Complete Records

You need a full record of all cryptocurrency transactions. This means noting the date and price when assets were acquired, traded, or exchanged. Relying on memory or partial data can lead to mistakes during tax filing; you may overlook some information. Having complete records simplifies the process for you and ensures accuracy.

-

File All Cryptocurrency Actions

The government wants you to report all taxable cryptocurrency activities, no matter how small they might be. Failing to do so by assuming that some actions can be overlooked is risky. The chances of getting caught with an incomplete filing have increased thanks to new tracking technologies.

-

Identify the Type of Transactions

Different types of transactions can be either income or capital gain. You must correctly categorize each one. Misclassifying can result in inaccurate tax filing. Making time to familiarize yourself with the different types helps prevent complications.

-

Choose Reputable Platforms and Databases

It’s crucial to opt for such platforms that can provide you with the history of the transaction and proper documentation for your transactions. Do not depend on unregistered platforms, especially if they’re offering no documentation. In case you have incomplete data, it will be difficult to report.

-

File Your Report on Time

It’s vital to file your report on time. Also, before submitting your report, it’s important to verify your data to ensure that everything is right and complete. Just one mistake can get you a fine easily avoided by verification.

Crypto tax compliance is no longer something you can delay or overlook. It requires basic record-keeping, accurate reporting, and careful review.

Doing it right not only helps you avoid penalties, but it also protects you from situations where confusion can be used against you.

Crypto Tax Scams and How Fake Demands Work

As crypto tax rules become clearer in 2026, more users expect tax-related steps. Scammers use this to create fake tax demands that appear at the right moment and feel real.

These scams usually begin on fake crypto platforms or fake investment platforms. In the beginning, everything looks normal. The platform shows your balance, your profits, and basic activity. In some cases, small withdrawals are even allowed. This builds trust.

The problem starts when you try to withdraw a larger amount. Instead of completing the request, the platform shows a message saying your withdrawal is on hold due to a tax requirement.

The message often looks official. It may include terms like “tax clearance,” “compliance,” or “verification.” Because users already expect taxes, the request feels like part of a normal process.

Many users pay at this stage to avoid delays or issues. Once the payment is made, the platform may ask for another fee or stop responding. In some cases, access to the account is blocked completely.

This is how the scam works: it appears normal until the moment you try to access your funds.

Now that you understand how these scams work, the next step is knowing how to spot them early.

Red Flags of Fake Crypto Tax Demands

Fake tax demands follow common patterns. Knowing these signs can help you stop before making a payment.

-

You Are Asked to Pay Tax Before Withdrawal

When a platform says you must pay tax to release your funds, this is a warning sign. Real tax systems do not require upfront payment to access your money.

-

The Message Feels Urgent

You may see messages saying your account will be blocked or your funds will be frozen if you do not act quickly. This pressure is used to rush your decision.

-

Payment Is Requested in Crypto

Being asked to pay tax in crypto, especially to a wallet address, is not normal. This is a strong sign of a scam.

-

No Clear Explanation or Proof

When the platform cannot clearly explain the charge or provide proper details, you should be cautious. Vague answers are a common pattern in scams.

-

More Payments Are Requested

After one payment, another fee may appear. This can continue until the user stops sending money.

-

Support Stops Responding

Once payments are made, the platform may delay replies or stop responding completely. In some cases, your account access may be restricted.

If you notice any of these signs, stop and do not make a payment. Taking a moment to check can help you avoid losing your funds.

Stay Compliant, Stay Protected

Crypto taxes in 2026 are more structured than before. The rules are clearer, and reporting is now expected from every user.

At the same time, scams are becoming more targeted. Many appear during withdrawals, where users are asked to make fake tax payments to access their funds.

This is where awareness matters most.

Understanding real tax rules makes it easier to spot what does not make sense. A platform asking for upfront tax, urgent payments, or repeated fees is not following a real process.

Staying compliant is not just about avoiding penalties. It also helps prevent situations where confusion is used against you.

In cases where funds have already been sent, reviewing the transaction history becomes important. This is where firms like Global Financial Recovery are often involved, helping trace transactions and assess next steps.

Taking action early, along with the right guidance, can improve the chances of recovering lost crypto funds and prevent further loss.

FAQs (Frequently Asked Questions)

The crypto tax rules in 2026 require users to report all taxable crypto activity, including selling, trading, and spending cryptocurrency. Income from staking, rewards, or airdrops must also be reported. In the U.S., updated reporting laws mean many exchanges now share transaction data with tax authorities, making accurate reporting more important than before.

Yes, all taxable crypto transactions must be reported, even small ones. This includes minor trades, swaps, or payments made using crypto. Ignoring small transactions can create gaps in your report, and with improved tracking systems, these gaps are easier to detect.

To avoid crypto tax penalties, keep clear records of every transaction, report all gains and income, and file your taxes on time. Make sure each transaction is correctly classified as capital gains or income. Using accurate data from reliable platforms reduces the risk of errors and penalties.

Yes, many exchanges now follow crypto exchange reporting laws and share user transaction data with tax authorities. In the U.S., this is part of updated broker reporting requirements. This means your trading activity may already be visible, so your tax report should match your actual transactions.

Fake crypto tax payment scams usually appear when a user tries to withdraw funds from a platform. The platform claims that a tax must be paid before the withdrawal can be processed. These demands often look official but are not real. Legitimate tax authorities do not require upfront payments through trading platforms, and such requests are a strong sign of a scam.

Book A Free Consultation

Recent Posts

Empowering you to reclaim what's rightfully yours. Together, we stand strong against financial fraud.